The Home Loan Process

Lynn Wiand

NMLS #: 394920

Mortgage Banker

First Merchants Bank

- 32991 Hamilton Ct., Farmington Hills, MI 48334

- C: (248)-228-4805

- LWiand@firstmerchants.com

I love what I do for my clients and partners! I have been a top producing woman in the financial industry for more than 30 years. I have helped thousands of people buy their first home, build their dream, buy a second home for family vacations and helped those downsizing. What I can provide is expertise, knowledge, understanding, a listening ear and compassion. What we as a team can provide is a hand to help you through from the initial prequalification to the day we sit together at the closing table. I have been the number one female loan officer in an industry made up of mostly men and always in the top five of producing loan officers for the companies with whom I have worked. We work with clients that are first time home buyers, clients that may have challenges that don’t allow them to qualify for conventional financing, new construction, FHA and VA clients, Doctor loans with zero down. These are just a few of the products we offer. Talk to us and find out how we can help you!

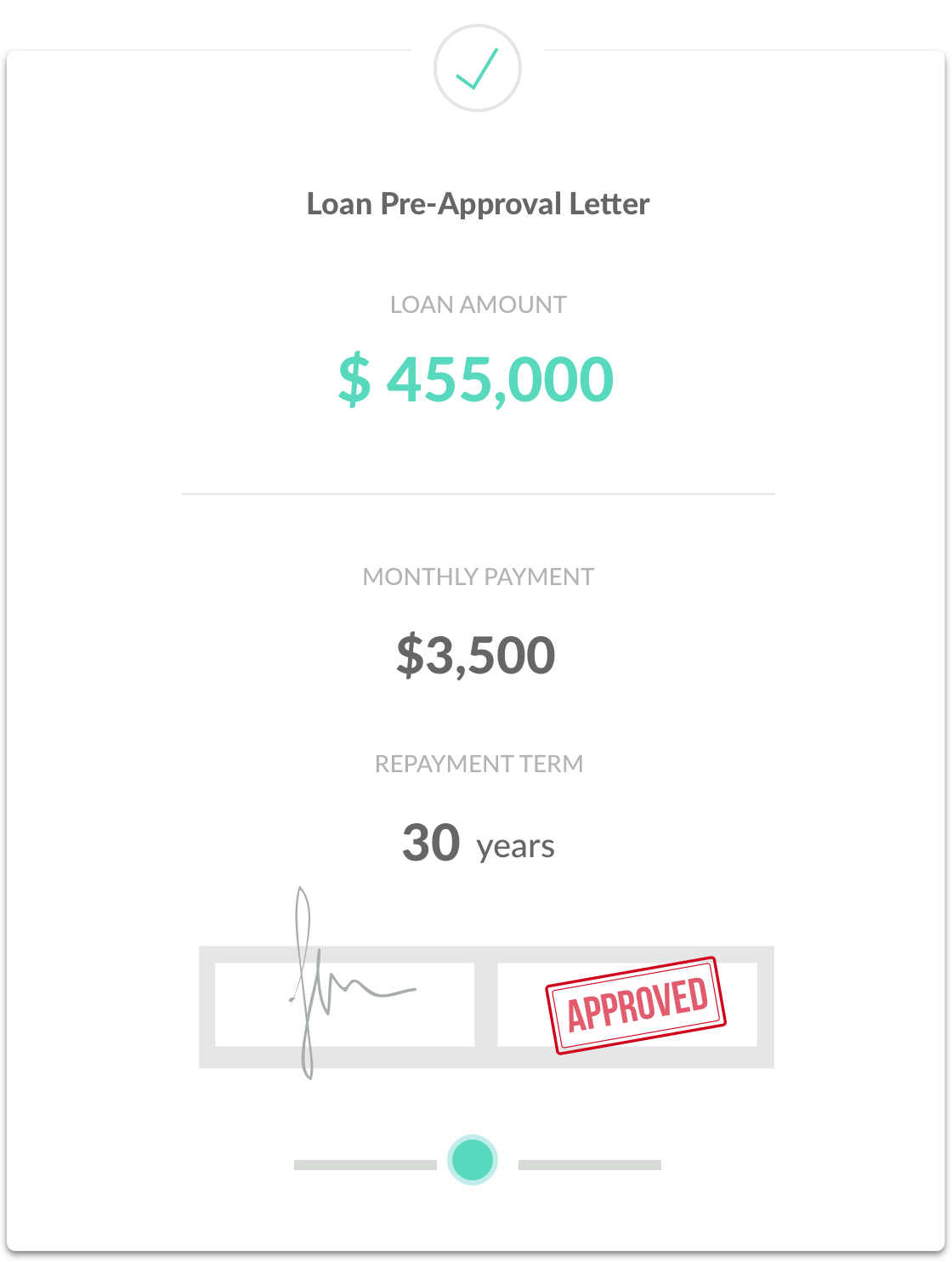

Get Pre-Approval

Before you start looking for a home to buy, it’s a good idea to meet with your Loan Officer to get pre-approved for a loan amount. At this stage, the lender gathers information about income, assets and debts of the borrower (you) to determine how much house you may be able to afford. This includes a credit report, W-2 forms, pay stubs, Federal Tax Returns and recent bank statements. There are a variety of different loan programs, so make sure to get pre-qualification for the specific programs that best suit your needs.

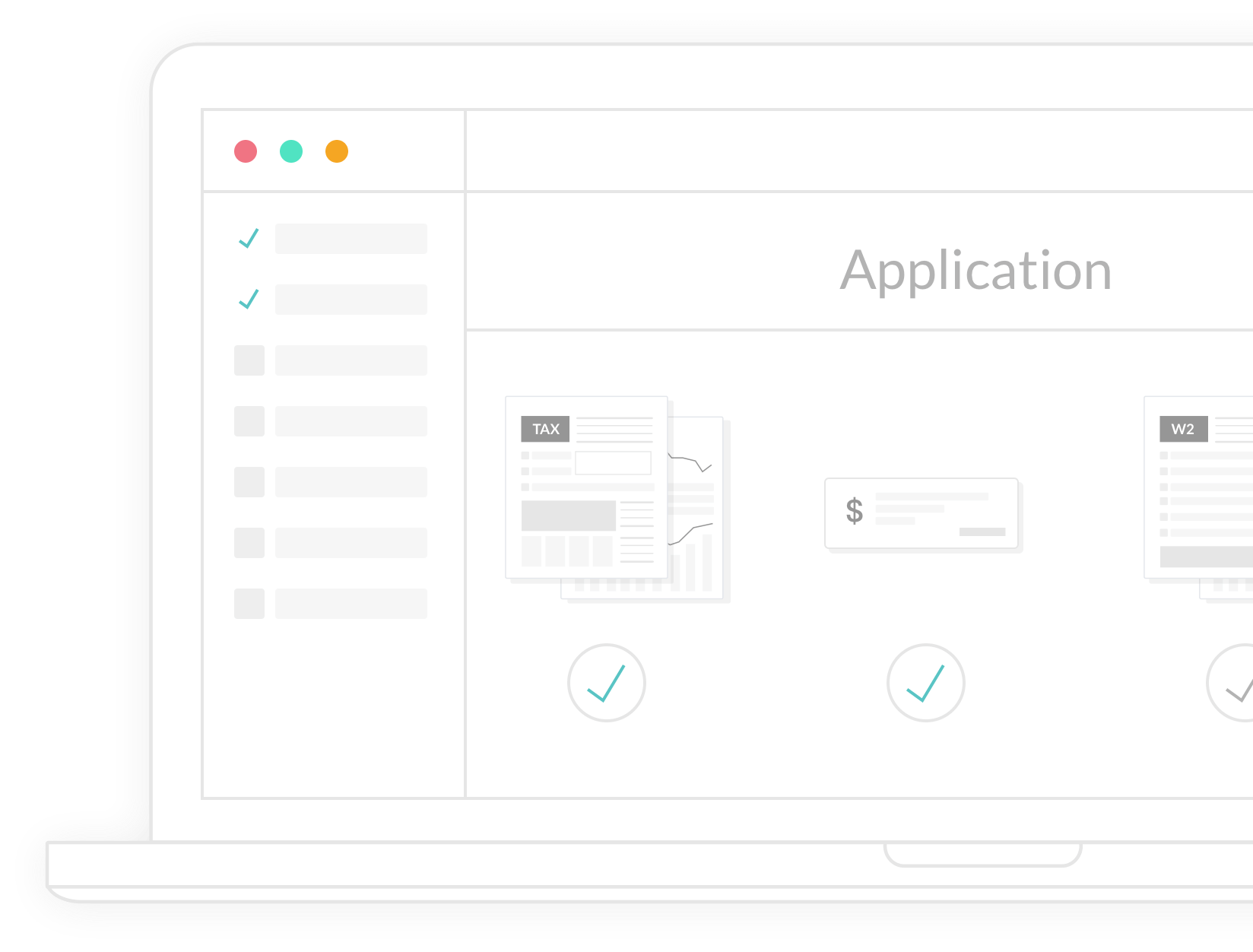

Application & Processing

What happens when a loan goes "live"

When you find property you’re ready to buy, your lender will help you complete a full mortgage loan application, and talk you through the various fees and down payment options. The application is submitted to processing, where the documents are reviewed and appraisals and title examination are ordered. Then the loan is sent to an underwriter, who reviews and approves the entire loan if it meets compliance.

Know Your Mortgage Payment

Based on the home's sale price, the term of the loan, buyer's down payment percentage, and the loan's interest rate, this calculator can help estimate what you'll need to pay out monthly for your new home. This calculator factors in PMI (Private Mortgage Insurance) for loans with less than a 20% down payment, as well as town property taxes and its effect on the total monthly mortgage payment.

Buying a home is a big step! Whether you're buying your first home, your dream home, or your tenth investment property, yours will be a big investment. We know how important this is to you and we have an army of experts to make sure we find the perfect property for your unique circumstances. Finding the perfect property is just one way we can help you with your real estate purchase.

In order to determine the amount of home you can afford a lender will use your debt-to-income ratio to determine the percentage of your pre-tax income you spend on debt. Your debt ratio will include: monthly housing costs, car payments, credit cards, student loans, and any other installment debt. If you take on more debt before buying a home it will have an impact on the amount of the loan that the lender will finance.

Closing

Signing and Finalizing the deal

Don’t be surprised if you’re asked for additional documentation or clarification throughout the process. Once your loan is approved, don’t forget to set up homeowners insurance. Your documents will be sent to the title company, where you’ll sign for the new home and pay any remaining costs. Then the loan is recorded and you get the keys. Congratulations, happy homeowner!

We Help You Get The Best Loan

Start The Process

We’ll help you find the best local loan officer to get you competitive rates and the programs that best fit your individual needs. Fill out this form and we’ll connect you with a lender today!